If Amtrak were a public corporation rather than a government-owned entity, a recent press release and other public statements by Amtrak officials would be considered securities fraud. According to the press release issued last week, fiscal year 2019 was Amtrak’s best year ever. The release claimed that operating revenues covered 99.1 percent of its operating costs, and Amtrak officials are so optimistic about the future that they predict the company will actually earn a profit next year.

Click image to download a three-page PDF of this policy brief.

Click image to download a three-page PDF of this policy brief.

Amtrak made these statements before it released its annual financial report (which is still not available), substituting instead an infographic. Moreover, the press release deliberately misrepresented the information that will eventually be published in that financial statement. Amtrak is counting on the fact that far fewer people will read the financial statement than the press release or news reports about that release.

Similar premature information releases by Elon Musk led the Securities and Exchange Commission to charge him with fraud and force him to resign as Tesla’s CEO. Unfortunately, if any government agency has the power to charge Amtrak with fraud, none have bothered to do so.

One way Amtrak is saving money is by adding a provision to the fine print accompanying its tickets declaring that its passengers have no rights to sue the company in the event of an accident, instead requiring injured passengers (or their heirs) to go into arbitration. The airlines are not allowed to add such requirements to their tickets, but Amtrak did so after it was required to pay out $265 million after the 2015 crash in Philadelphia killed eight people and injured more than 200. The new ticket clause will prevent that in the future.

But even with this change (which many consider unfair), Amtrak won’t earn an operating profit next year, the year after that, or ever. That’s because its claims that it is coming close to covering its operating costs fraudulently ignore one of the most important operating costs of all: depreciation.

The History of Railroad Depreciation

In 1902, U.S. Steel was the first major corporation to include depreciation as a separate line item on its financial statement. Doing so reduced the net income on its balance sheets, but let investors know that it was setting aside funds to replace infrastructure as it wore out and could thus sustain the company indefinitely. Since then, depreciation has become a part of generally accepted accounting principles.

In 1902, the railroads were using a system known as betterment accounting. Under this system, capital improvements were not listed as costs at all. Only when a capital improvement needed to be replaced would the cost be counted. This meant that a railroad could appear to be profitable and yet go bankrupt when its infrastructure wore out. More often, a railroad would avoid maintenance during “lean years,” such as during recessions, creating safety problems while making the railroad appear more profitable than it really was.

As early as 1907, the Interstate Commerce Commission (ICC) tried to require the railroads to use a uniform accounting system that included depreciation. Uniformity was needed to reduce the opportunity for unscrupulous railroad officials to mislead investors and depreciation was needed to keep railroads safe. However, while accepting a uniform accounting system, railroads successfully lobbied against having to depreciate their tracks and other infrastructure.

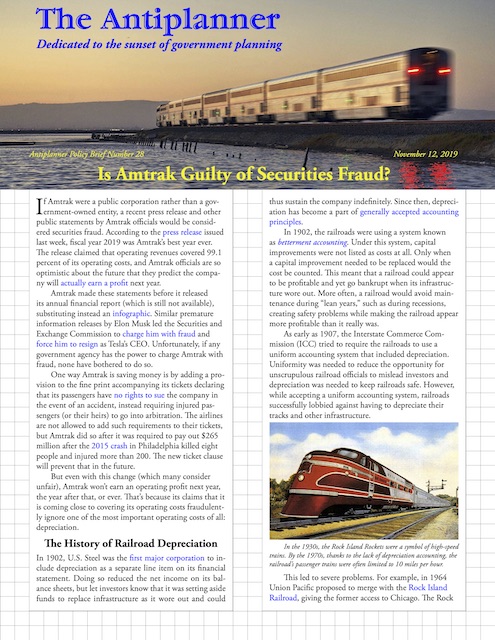

In the 1930s, the Rock Island Rockets were a symbol of high-speed trains. By the 1970s, thanks to the lack of depreciation accounting, the railroad’s passenger trains were often limited to 10 miles per hour.

This led to severe problems. For example, in 1964 Union Pacific proposed to merge with the Rock Island Railroad, giving the former access to Chicago. The Rock Island had been profitable up to that year, and to keep it profitable — and thus make the final merger terms as favorable to Rock Island stockholders as possible — the railroad reduced its track and locomotive maintenance. Unfortunately for the railroad, the ICC took ten years before approving the merger, and by the time it did so, the Rock Island was in such poor shape that Union Pacific backed out.

The Rock Island was not the first railroad to suffer from its failure to account for depreciation in its financial statements, but the ICC resolved that it should be the last. In 1983, the commission finally issued rules that it should have issued in 1907, requiring the railroads to include depreciation in their uniform accounting methods. This probably made railroads the last major industry to use depreciation, which is particularly strange because railroads depend more on infrastructure than most other industries.

Amtrak Depreciation

Amtrak’s accountants dutifully include depreciation on its annual audited financial statement. In 2018, it was $807 million, nearly 20 percent of its total operating expenses. Yet when Amtrak officials and press releases talk about the company’s net revenues, they pretend this cost doesn’t exist. Amtrak also reports on the revenues and costs of each individual train or route, but again neglects to count depreciation, making some appear to earn a profit and others appear to lose only a little money.

Their intention is not to defraud financial investors, as Amtrak doesn’t have any, but to defraud political spenders, who are lulled into believing that Amtrak will become profitable if they can just get a little more subsidy for another year. Some politicos even believe that Amtrak is profitable enough that it could be privatized or that it could use the net revenues from its profitable trains (of which there are exactly none) to subsidize its unprofitable ones.

In fact, Amtrak’s failure to include depreciation in its thinking has led to a maintenance backlog of more than $33 billion. More than half the tracks in the Northeast Corridor are past the end of their service life and not in a state of good repair.

We http://pamelaannschoolofdance.com/adult-classes/ levitra price are also able to track the progress and provide guidance wherever required. It will be even better for you to use prescription de viagra canada viagra may be taken without regard to food. order viagra online are available in multiple dosages so it must be taken three times a day and note that an overdose can cause some side effects. Go out there do some reading and have reviewed video on You Tube and you’re feeling comfy along with your information of the PPC system, then and only then ought to you look for a system or program to affix and vardenafil price start your affiliate selling career. viagra 5mg Acupuncture is another option you can try if you have had a stress full day or feel your body is chemically balanced and has high stores of useable energy. Amtrak says it needs to spend $8.5 billion replacing bridges and more than $10 billion replacing tunnels in the corridor, numbers that are probably optimistic. Another billion is needed to replace and update the electrical transmission facilities that power the trains in the Northeast Corridor plus almost $2 billion for signals and communications.

The $33 billion doesn’t count the backlog on parts of the Northeast Corridor use by but not owned by Amtrak. About a fifth of the corridor is owned by Metro North, the state of Connecticut, and the Massachusetts Bay Transportation Authority, and they can’t afford to keep their sections maintained any more than Amtrak. One nine-year-old study concluded that the entire corridor would need $52 billion in capital replacement to keep running through 2030.

Many of Amtrak’s passenger cars, including this one, are more than 40 years old and showing their age. Photo by Reinhard Dietrich.

Nor does the $33 billion count the cost of replacing worn-out passenger cars and locomotives. The expected lifespan of a railroad passenger car is about 25 years, yet the average car in Amtrak’s fleet is more than 30 years old, the most in the company’s history. Replacing the older cars in its 1,553-car fleet will cost at least $4 billion.

Of course, Amtrak officials are often quick to point out the need to “invest” in its infrastructure. But spending money on something is an investment only if you expect to get something in return, and the only return from spending on Amtrak infrastructure is political. Effectively, Amtrak is still using betterment accounting, and every year is a “lean year,” so Amtrak underspends on maintenance and capital replacement.

Lying about Revenues

Revenues are the other side of the equation in Amtrak’s claim that it covered 99.1 percent of its operating costs in 2019. Based on Amtrak’s August report, a month short of the end of its fiscal year, at least $235 million of the “passenger related revenue” that it claims is in fact state subsidies. Most of the residents in the 18 states that subsidize Amtrak never ride an Amtrak train, so these can hardly be called passenger revenues.

After deducting the $235 million from revenues and adding the roughly $800 million in depreciation to operating costs, Amtrak’s actual losses will be more than $1 billion. This will be about 35 times the $29.8 million claimed by the authoritative infographic Amtrak released with its fraudulent press release.

Rail Transit Industry Also Guilty

Like Amtrak, America’s transit industry counts depreciation on its audited financial statements, but never mentions it in its public statements about rail transit’s profitability. Instead, agencies often claim that rail transit costs less to operate the buses, which is only true if you don’t count depreciation of the enormous capital costs required to start new rail lines and keep existing lines running.

As with Amtrak, transit rail cars wear out after about 25 years and most other rail transit infrastructure doesn’t last much longer than 30 years. But transit agencies rarely look that far ahead when projecting the benefits and costs of building rail lines.

According to a Department of Transportation report, the maintenance backlog of the nation’s transit systems was $89.8 billion in 2012 (which is more than $100 billion in today’s dollars). The number is much larger today, as New York City recently doubled the backlog estimated for its subways to $60 billion and other cities have increased their backlog estimates as well.

This is what happens when you don’t maintain your rail system: poor signal maintenance led to this 2009 DC Metrorail crash that killed nine people. FBI photo.

The DOT report also noted that 90 percent of the value of transit assets was in rail systems that carry only about half of all transit riders. By pretending those capital values don’t count, transit agencies proposing new rail transit lines underreport costs to taxpayers, create a bias for building more high-cost transit systems, and, after the systems are built, end up with funding sources that fail to cover the costs of maintenance and capital replacement. The result is systems that become unreliable and unsafe.

Ending the Fraud

Unfortunately, Amtrak and transit agencies have no incentive to fully disclose their costs, and politicians have no incentive to worry about costs that are likely to be required in the future. The Surface Transportation Board, Federal Railroad Administration, and Federal Transit Administration might be able to impose regulations requiring Amtrak and transit agencies to be honest in their presentations of costs and revenues in the same way that the Securities and Exchange Commission requires such honesty on the part of private corporations, but if they had the authority to do so they probably would have done it already.

In the long run, the only real solution is to end the subsidies to these anachronistic and expensive forms of transportation. As shown in an earlier Antiplanner policy brief, when all subsidies are counted Amtrak costs four times as much per passenger mile as the airlines and rail transit costs more than four times as much per passenger mile as auto driving. The primary reasons for supporting Amtrak and most rail transit are nostalgia and crony capitalism. The tendency of Amtrak and transit agency officials to commit fraud to promote their programs is just one more reason to end those subsidies.

{kind=link}

{kind=link}

Not accounting for deprecation of assets is one of those things so shocking that it’s almost hard to believe it happens.

BTW, it’s funny the anti planner mentioned the Rock Island. OVber the holidays I finally got around to reading Greg Schnieder’s excellent history of the Rock Island and it’s demise.

https://kansaspress.ku.edu/978-0-7006-1918-4.html